Solving a finite-horizon semi-MDP

Lars Relund lars@relund.dk

2026-06-22

Source:vignettes/finite-mdp.Rmd

finite-mdp.RmdThe MDP2 package in R is a package for solving Markov

decision processes (MDPs) with discrete time-steps, states and actions.

Both traditional MDPs (Puterman 1994),

semi-Markov decision processes (semi-MDPs) (Tijms

2003) and hierarchical-MDPs (HMDPs) (Kristensen and Jørgensen 2000) can be solved

under a finite and infinite time-horizon.

The package implement well-known algorithms such as policy iteration

and value iteration under different criteria e.g. average reward per

time unit and expected total discounted reward. The model is stored

using an underlying data structure based on the state-expanded

directed hypergraph of the MDP (Nielsen and

Kristensen (2006)) implemented in C++ for fast

running times.

Building and solving an MDP is done in two steps. First, the MDP is built and saved in a set of binary files. Next, you load the MDP into memory from the binary files and apply various algorithms to the model.

For building the MDP models see vignette("building"). In

this vignette we focus on the second step, i.e. finding the optimal

policy. Here we consider a finite-horizon semi-MDP.

A finite-horizon semi-MDP

A finite-horizon semi-MDP considers a sequential decision problem over stages. Let denote the finite set of system states at stage . When state is observed, an action from the finite set of allowable actions must be chosen, and this decision generates reward . Moreover, let denote the stage length of action , i.e. the expected time until the next decision epoch (stage ) given action and state . Finally, let denote the transition probability of obtaining state at stage given that action is chosen in state at stage .

Example

Consider a small machine repair problem used as an example in Nielsen and Kristensen (2006) where the machine is always replaced after 4 years. The state of the machine may be: good, average, and not working. Given the machine’s state we may maintain the machine. In this case the machine’s state will be good at the next decision epoch. Otherwise, the machine’s state will not be better at next decision epoch. When the machine is bought it may be either in state good or average. Moreover, if the machine is not working it must be replaced.

The problem of when to replace the machine can be modeled using a

Markov decision process with

decision epochs. We use system states good,

average, not working and dummy state

replaced together with actions buy (buy),

maintain (mt), no maintenance (nmt), and

replace (rep). The set of states at stage zero

contains a single dummy state dummy representing the

machine before knowing its initial state. The only possible action is

buy.

The cost of buying the machine is 100 with transition probability of

0.7 to state good and 0.3 to state average.

The reward (scrap value) of replacing a machine is 30, 10, and 5 in

state good, average and

not working, respectively. The reward of the machine given

action mt are 55, 40, and 30 in state good,

average and not working, respectively.

Moreover, the system enters state 0 with probability 1 at the next

stage. Finally, the reward, transition states and probabilities given

action

nmt

are given by:

good

|

average

|

good

|

average

|

good

|

average

|

|

|---|---|---|---|---|---|---|

| 70 | 50 | 70 | 50 | 70 | 50 | |

Let us try to load the model and get some info:

prefix <- paste0(system.file("models", package = "MDP2"), "/machine1_")

mdp <- load_mdp(prefix)#> Read binary files (0.000235417 sec.)

#> Build the HMDP (3.7876e-05 sec.)#> Checking MDP and found no errors (3.875e-06 sec.)

get_info(mdp, with_list = F, df_level = "action", as_strings_actions = TRUE)#> $df

#> # A tibble: 18 × 9

#> s_id state_str label a_idx label_action weights trans_weights trans pr

#> <dbl> <chr> <chr> <dbl> <chr> <chr> <lgl> <chr> <chr>

#> 1 4 3,0 good 0 mt 55 NA 0 1

#> 2 4 3,0 good 1 nmt 70 NA 0,1 0.2,0.8

#> 3 5 3,1 average 0 mt 40 NA 0 1

#> 4 5 3,1 average 1 nmt 50 NA 1,2 0.2,0.8

#> 5 6 3,2 not working 0 mt 30 NA 0 1

#> 6 6 3,2 not working 1 rep 5 NA 3 1

#> 7 7 3,3 replaced 0 Dummy 0 NA 3 1

#> 8 8 2,0 good 0 mt 55 NA 4 1

#> 9 8 2,0 good 1 nmt 70 NA 4,5 0.5,0.5

#> 10 9 2,1 average 0 mt 40 NA 4 1

#> 11 9 2,1 average 1 nmt 50 NA 5,6 0.5,0.5

#> 12 10 2,2 not working 0 mt 30 NA 4 1

#> 13 10 2,2 not working 1 rep 5 NA 7 1

#> 14 11 1,0 good 0 mt 55 NA 8 1

#> 15 11 1,0 good 1 nmt 70 NA 8,9 0.6,0.4

#> 16 12 1,1 average 0 mt 40 NA 8 1

#> 17 12 1,1 average 1 nmt 50 NA 9,10 0.6,0.4

#> 18 13 0,0 Dummy 0 buy -100 NA 11,12 0.7,0.3The state-expanded hypergraph representing the semi-MDP with finite time-horizon can be plotted using

plot(mdp, action_color = "label", radx = 0.06, mar_x = 0.065, mar_y = 0.055)

Each node corresponds to a specific state and a directed hyperarc is

defined for each possible action. For instance, action mt

(maintain) corresponds to a deterministic transition to state

good and action nmt (not maintain) corresponds

to a transition to a condition/state not better than the current

condition/state. We buy the machine in stage 1 and may choose to replace

the machine.

Let us use value iteration to find the optimal policy maximizing the expected total reward:

scrapValues <- c(30, 10, 5, 0) # scrap values (the values of the 4 states at the last stage)

run_value_ite(mdp, "Net reward", term_values = scrapValues)#> Run value iteration with epsilon = 0 at most 1 time(s)

#> using weight 'Net reward' under expected-weight Bellman operator.

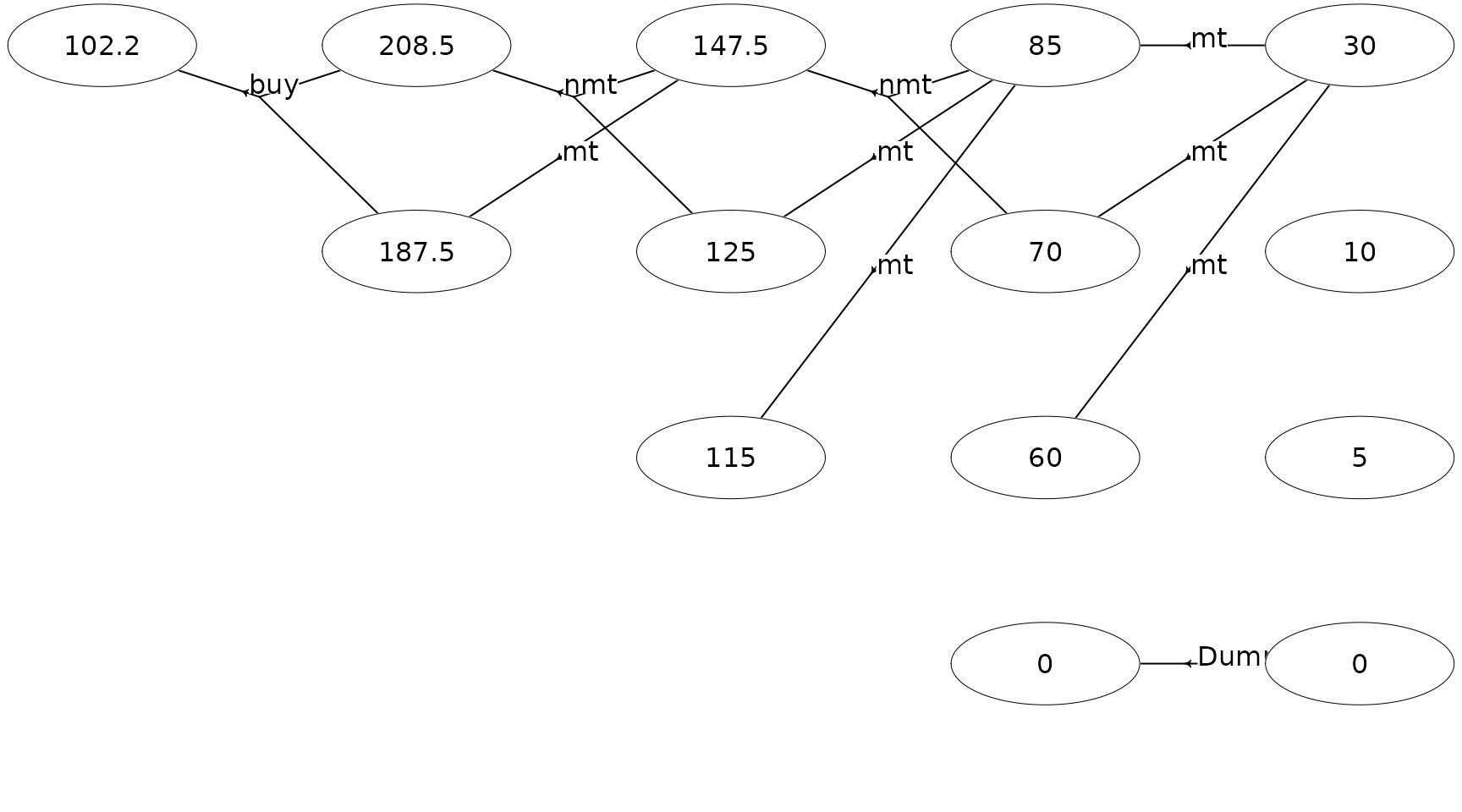

#> Finished. Cpu time 9.194e-06 sec.The optimal policy is:

pol <- get_policy(mdp)

tail(pol)#> # A tibble: 6 × 6

#> s_id state_str state_label a_idx action_label weight

#> <dbl> <chr> <chr> <int> <chr> <dbl>

#> 1 8 2,0 good 1 nmt 148.

#> 2 9 2,1 average 0 mt 125

#> 3 10 2,2 not working 0 mt 115

#> 4 11 1,0 good 1 nmt 208.

#> 5 12 1,1 average 0 mt 188.

#> 6 13 0,0 Dummy 0 buy 102.

plot(mdp,

actions_visible = "policy", state_label = "weight",

radx = 0.06, mar_x = 0.065, mar_y = 0.055

)

Note given the optimal policy the total expected reward is 102.2 and

the machine will never make a transition to states

not working and replaced.

We may evaluate a certain policy, e.g. the policy always to maintain the machine:

policy <- data.frame(s_id = c(8, 11), a_idx = c(0, 0)) # set the policy for s_id 8 and 11 to mt

set_policy(mdp, policy)

get_policy(mdp)#> # A tibble: 14 × 6

#> s_id state_str state_label a_idx action_label weight

#> <dbl> <chr> <chr> <int> <chr> <dbl>

#> 1 0 4,0 good -1 "" 30

#> 2 1 4,1 average -1 "" 10

#> 3 2 4,2 not working -1 "" 5

#> 4 3 4,3 replaced -1 "" 0

#> 5 4 3,0 good 0 "mt" 85

#> 6 5 3,1 average 0 "mt" 70

#> 7 6 3,2 not working 0 "mt" 60

#> 8 7 3,3 replaced 0 "Dummy" 0

#> 9 8 2,0 good 0 "mt" 148.

#> 10 9 2,1 average 0 "mt" 125

#> 11 10 2,2 not working 0 "mt" 115

#> 12 11 1,0 good 0 "mt" 208.

#> 13 12 1,1 average 0 "mt" 188.

#> 14 13 0,0 Dummy 0 "buy" 102.If the policy specified in set_policy does not contain

all states then the actions from the previous optimal policy are used.

In the output above we can see that the policy now is to maintain

always. However, the reward of the policy has not been updated. Let us

calculate the expected reward:

run_calc_weights(mdp, "Net reward", term_values = scrapValues)

tail(get_policy(mdp))#> # A tibble: 6 × 6

#> s_id state_str state_label a_idx action_label weight

#> <dbl> <chr> <chr> <int> <chr> <dbl>

#> 1 8 2,0 good 0 mt 140

#> 2 9 2,1 average 0 mt 125

#> 3 10 2,2 not working 0 mt 115

#> 4 11 1,0 good 0 mt 195

#> 5 12 1,1 average 0 mt 180

#> 6 13 0,0 Dummy 0 buy 90.5That is, the expected reward is 90.5 compared to 102.2 which was the reward of the optimal policy.